2Q 2026 Investment Letter

July 2, 2026

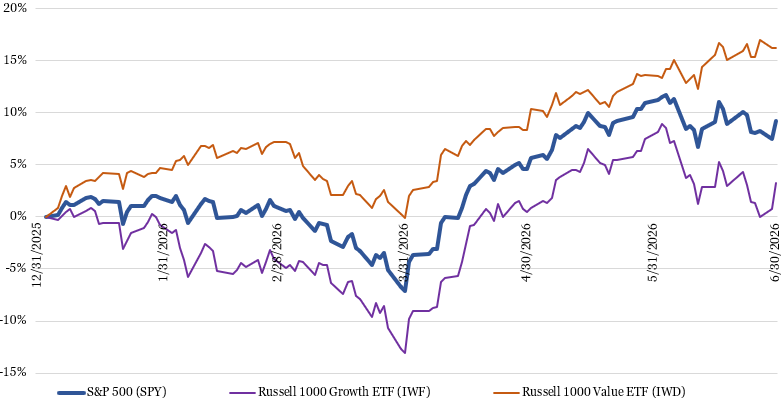

The second quarter of 2026 served as an important reminder that financial markets are forward looking. While investors entered the quarter focused on the ongoing Iran conflict, elevated energy prices, and consumer weakness at the bottom of the K-shaped economy, the market steadily looked beyond those headlines. As fears of a prolonged disruption to global commodity supplies eased and the probability of a worst-case scenario diminished, equities staged a powerful recovery. All told, the S&P 500 (SPY) increased by 15.1%, its best quarter since the second quarter of 2020.

Figure 1: Markets Staged a Powerful Rally in the Second Quarter

Source: Koyfin (inclusive of dividends)

Market leadership shifted noticeably. The defensive sectors that outperformed during the first quarter — energy, materials, consumer staples, and utilities — gave back some of their relative strength as investor risk appetite improved. Meanwhile, the big five hyperscalers that are spending massive sums on artificial intelligence (AI) infrastructure spending — Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOG), Meta Platforms (META) and Oracle (ORCL) — also underperformed the broader market given concerns on what kind of returns they will ultimately generate from that spend.

As the hyperscalers laid out ambitious spending plans for this year and next, investors’ dollars rotated back toward companies on the receiving end of the spending, particularly semiconductors, memory and storage names. Major bottlenecks have emerged in the AI ecosystem, giving companies that sell supply-constrained products tremendous pricing power that is supercharging their earnings. Further, investors have grown increasingly confident the AI investment cycle remains in the early stages and more willing to pay a higher valuation multiple on near-term earnings.

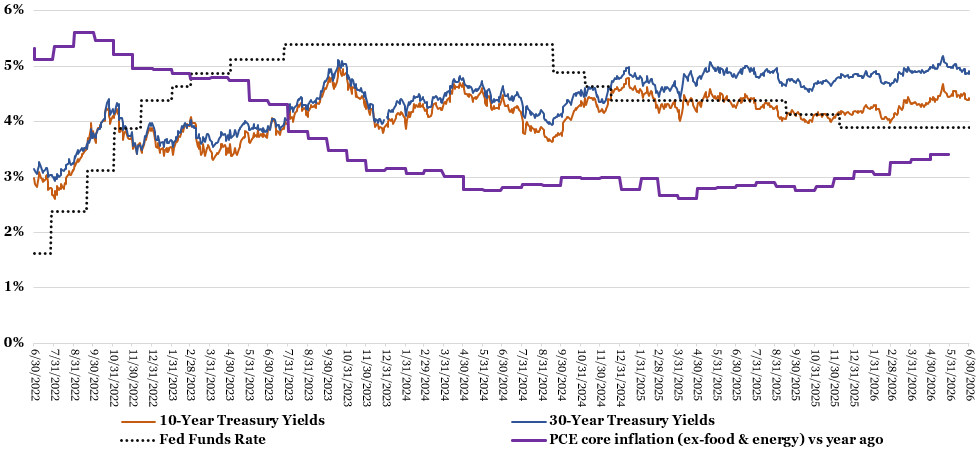

Economic fundamentals remained constructive. The labor market continued to demonstrate resilience despite moderating hiring activity, consumer spending generally held up well, and corporate profitability margins remained elevated. At the same time, inflation worries moderated as crude oil prices retreated substantially from their April highs following signs of stabilization in the Middle East and improving expectations surrounding energy supply. The feared combination of accelerating inflation and weakening growth just did not materialize during the quarter.

Interest rates nevertheless remain an important variable. Earlier this year, many investors anticipated additional Federal Reserve rate cuts during 2026 under President Trump-appointed new Federal Reserve Chairman Kevin Warsh. Instead, persistent economic resilience and renewed inflation concerns have led markets to reassess that outlook. During Warsh’s first press conference as chairman on June 17th, he held a decidedly more hawkish tone, seemingly less likely to heed Trump’s prior clamoring for the Fed to lower rates. Fed funds futures now imply the Fed is likely to raise rates once or twice this year, with September currently viewed as the most probable meeting for a quarter-point increase.

Figure 2: Inflation Back on the Rise but Rates Tame

Sources: St. Louis Fed/Board of Governors of the Federal Reserve System. https://fred.stlouisfed.org/series/DGS10 (10-year US Treasury yield). https://fred.stlouisfed.org/series/DGS30 (30-year US Treasury yield) https://fred.stlouisfed.org/series/PCEPILFE (PCE inflation ex-food & energy). Forbes Advisor. https://www.forbes.com/advisor/investing/fed-funds-rate-history/ (Fed Funds rate).

Market Outlook

Although the geopolitical backdrop remains uncertain, the possibility of a prolonged closure of the Strait of Hormuz appears considerably less likely today than it did a few months ago. While geopolitical developments can always surprise investors, markets have largely shifted their focus back toward the trajectory of AI investment, corporate earnings, economic growth, and Fed policy.

Arguably the largest determinant for stock performance in the second half of the year will be the trajectory of the AI infrastructure buildout. Investors will be intensely focused on hyperscalers’ June quarter earnings reports, especially their updated guidance on capital expenditures. If hyperscalers signal any restraint on AI spending, then their shares ought to rebound and the ‘AI is destroying software’ narrative should ease, but AI infrastructure stocks could get crushed. Alternatively, if the AI spending spree continues unabated, then the market’s view of AI winners and losers ought to remain the same.

The second half of the year also brings the uncertainty historically associated with midterm election years. These years have historically been the worst of the presidential cycle, with the S&P 500 finishing the year higher just 53% of the time with an average gain of 4.6%, with the other three years finishing up 78% of the time, with an average gain of 11%. It is possible that much of the market-friendly tax and regulatory changes by the current administration have already been priced into the stock market over the past couple of years, ultimately leading to below average returns this year despite the strong first half start.

As I continue to say, successfully timing the stock market on a consistent basis is extraordinarily difficult. The first half of 2026 provided another excellent example. Investors who reacted emotionally to the Middle East conflict would have missed the best quarterly market performance in six years. Although risks undoubtedly remain — including sustainability of AI spending, elevated valuations, and the path of interest rates — I continue to believe that investors are best served by adhering to a long-term asset allocation that aligns with their individual return objectives, risk tolerance, and investment horizon.

Client Positioning

I take a long-term view that focuses on compounding returns in a tax-efficient manner. I allocate the bulk of my clients’ equity exposure to “quality growth” companies that possess durable competitive advantages, above-average long-term growth prospects, high levels of profitability and free cash flows, and prudent levels of debt. I generally take a “pruning the weeds and nurturing the flowers” approach of selling stocks that violate my investment thesis and retaining stocks of companies with solid fundamentals. I believe this investment philosophy affords my clients the best shot of generating maximum after-tax, risk-adjusted returns compounded over the long run.

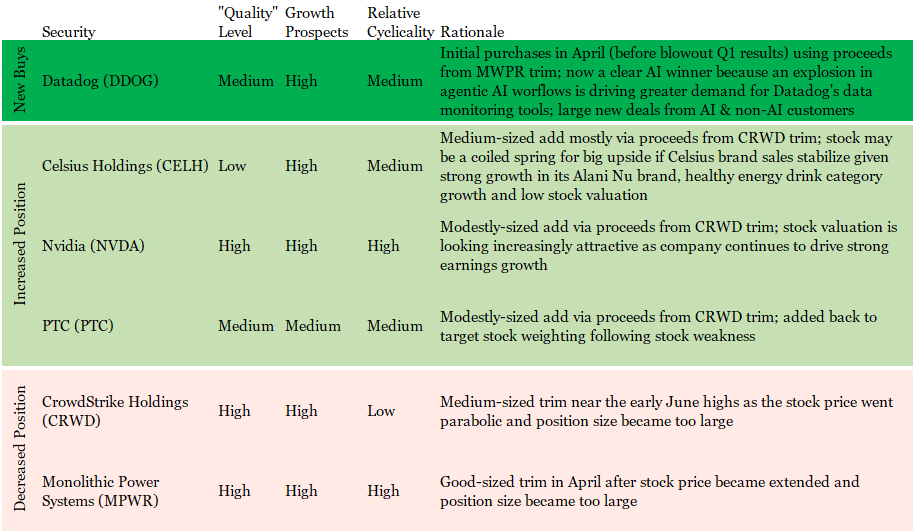

Portfolio activity was moderate during the second quarter and centered around two repositioning trades. The first involved trimming semiconductor company Monolithic Power Systems (MPWR) in April after a sharp rally pushed the stock to new highs and made it one of the largest holdings for many clients. I used those proceeds to initiate a position in Datadog (DDOG), a software company that monitors performance for applications. I bought DataDog because I wanted to take advantage of the false narrative that AI was going to negatively impact every software company. Based on my research, I surmised that Datadog could be a standout AI beneficiary. That thesis was quickly validated as the company reported strong first-quarter earnings and raised its financial outlook several weeks later.

The second repositioning trade occurred in early June when I trimmed cybersecurity company CrowdStrike Holdings (CRWD) after its shares nearly doubled in less than two months. Although I remain constructive on CrowdStrike's long-term growth prospects, the stock had become rather expensive. I redeployed those proceeds across several existing positions based on individual client weightings, with energy drink company Celsius Holdings (CELH) receiving the largest aggregate addition.

Figure 3: Portfolio Changes in Majority of Client Accounts in 2Q 2026

Source: Glass Lake Wealth Management

The degree of share price appreciation across many of the AI spending beneficiaries is cause for concern, as stock prices could dramatically reverse course on any negative industry headlines or if elevated expectations for each company are not reached. I intend to reduce clients’ exposure to AI spending winners further if shares continue to make new highs. In particular, I will monitor chipmaker Advanced Micro Devices (AMD) as client positions cross the one-year holding threshold in August, allowing for any gains in taxable accounts to be taxed at the lower long-term capital gains rate.

Because many have inquired on the SpaceX (SPCX) IPO, I am sharing my thoughts here. I did not seek to participate in the largest IPO of all-time because although I thought its Starlink business is a fantastic business with major growth potential and a wide economic moat, I believed the overall company was overvalued amid the hype, massive spending on its xAI business would drive years of losses, and the unlocking of insider sale restrictions over the first 180 days post-IPO would represent a meaningful stock headwind. This fall’s possible IPO of Anthropic, owner of large language model Claude, may be more intriguing.

I watched traditional energy stocks rise in the first quarter and fall in the second quarter from the sidelines. I put energy stocks in the long-term challenged bucket, alongside other more commoditized and hyper-competitive industries like airlines and automobile manufacturers. I also continue to avoid the most speculative areas of the market such as unprofitable “story” stocks, recent special purpose acquisition company (SPACs) offerings and pump-and-dump meme stocks.

For clients’ fixed income portfolios, I continue to focus on short to medium duration holdings (duration is a measure of a bond price’s sensitivity to changes in interest rates; when interest rates rise, bond prices fall). I want to abstain from high duration bonds because I do not believe long-term Treasury yields adequately reflect the United States’ difficult fiscal situation and monetary policy risks if a Warsh-led Fed proves to prioritize economic growth over fighting inflation.

Have a wonderful 4th of July and a happy, healthy, and wealthy remaining summer!

Sincerely,

Jim Krapfel, CFA, CFP

Founder/President

Glass Lake Wealth Management, LLC

glasslakewealth.com

608-347-5558

Disclaimer

Advisory services are offered by Glass Lake Wealth Management LLC, a Registered Investment Advisor in Illinois and North Carolina. Glass Lake is an investments-oriented boutique that offers a wide spectrum of wealth management advice. Visit glasslakewealth.com for more information.

This investment letter expresses the views of the author as of the date indicated and such views are subject to change without notice. Glass Lake has no duty or obligation to update the information contained herein. Further, Glass Lake makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, whenever there is the potential for profit there is also the possibility of loss.

This investment letter is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory, legal, or accounting services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends or market statistics is based on or derived from information provided by independent third-party sources. Glass Lake Wealth Management believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions in which such information is based.